Module component prices and ocean freight rates surged in 2020 due to increased demand for Chinese goods and a pandemic container shortage. In the face of rising cost pressures, module manufacturers lowered utilization rates and postponed delivery during and after the Lunar New Year. Prices for most module components began to fall, as suppliers ramp up new capacity and module manufacturers cut capacity utilization.

Prices for silver paste, however, have remained stubbornly high. Since silver has many industrial uses, and is a precious metal used as an investment in itself, it is subject to changes in supply and demand as well as market speculation.

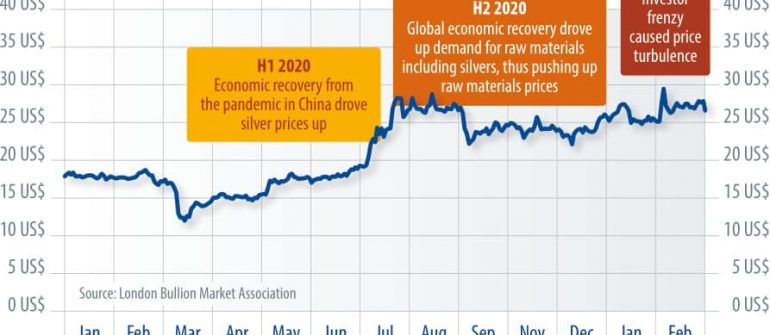

Price fluctuations

Silver prices surged at the end of January as investor frenzy swept the markets. iShares Silver Trust (SLV), the largest exchange-traded fund that tracks silver, recorded a price as high as $26.70 per ounce. Silver futures prices also rose to $29.90. Amid the price hikes CBOE Silver ETF Volality (VXSLV) made a jump to $82.3. Retail frenzy also caused the London Bullion Market Association’s (LBMA) silver spot price to reach nearly $30 see chart below). The LBMA silver prices are now the index for silver paste suppliers’ purchase of silver.

Paste costs

Silver is mainly used in manufacturing silver paste for solar cell metallization. P-type PERC technology, having hit a bottleneck in driving cell efficiencies further, now relies on the advancement of silver pastes. LBMA silver spot prices are used by silver paste suppliers and cell manufacturers as reference point during negotiations. In other words, processing costs and silver content in the paste also play a role, but silver spot price movement will directly affect the manufacturing costs of PV cells.

Silver paste prices have changed along with the LBMA silver spot price curve. Increases in silver paste price in the second half of 2020 not only pushed the costs of cells up, but also the share of silver paste in the non-silicon costs of cell production.

It is difficult to predict price movements in silver. Factors including economic trends, interest rates, and exchange rates all contribute to these price fluctuations. Under proper temperature and humidity conditions, silver pastes can be preserved for up to six months, and it usually takes suppliers at least a few months to introduce new silver pastes to help boost cell efficiencies.

With advantages in price negotiation and silver paste’s aforementioned features, cell manufacturers and vertically integrated companies do not need to stock up on silver pastes or draw inventory in advance, despite silver price movements. Instead, they can increase purchase frequency to spread the risk of silver price fluctuations to each purchase.

Price hikes

While silver is subject to speculation in the future, the market is big and the exchange has sufficient reserves for large short-term trading. Therefore, any speculation in the future will be short-lived. PV technology relies largely on silver pastes to improve cell efficiencies, and n-type TOPCon and HJT both require higher consumption of silver pastes. Calculating on the basis of M6 (166mm) wafers, the silver paste consumption of TOPCon cells is 50-75% higher, and HJT 200% higher, than a PERC cell. The low-temperature silver paste required to process HJT cells is also more expensive.

Once cell manufacturers and vertically integrated companies ramp up gigawatt-scale n-type cell capacity expansions, the consumption of silver paste and cost control will become issues. As the global economy rebounds from the Covid-19 recession, demand for silver will rise significantly from PV and the many other industries where the material is used.

A fast economic recovery will drive up silver prices in the long term. Global inflation collapsed last year due to the economic slump and sluggish oil prices, but it is likely to bounce back rapidly this year, thanks to a strong economic recovery and last year’s low base. By then, demand for precious metals such as gold and silver that can be used to hedge against inflation will rise, and this will push silver prices higher.

In the wake of the pandemic, PV demand looks bright as countries across the globe launch ambitious climate targets and postponed projects are getting off the ground. PV InfoLink expects module demand to reach 153.8 GW this year, up 10% compared with 2020.

In terms of PERC cells larger than 166 mm, production output is expected to hit 130 GW by the end of the year. N-type cells, led by Longi, Jinko and Tongwei’s GW-scale capacity expansion, are estimated to see 6 GW of production. As demand for silver pastes will grow steadily, silver price movement will have a bigger impact on costs for PV manufacturers.

Maintaining balance between utilization rates and cost control will become a major issue facing manufacturers amid large-scale capacity expansion and increases in raw materials costs.